ITR FILING for FREELANCERS: All about Compliances

Freelancers can work freely, decide their employment, and make money without being restricted by an employer when they work independently. But this independence also means that you have to handle your taxes on your own. Freelancers do not have an employer to withhold and deposit taxes, in comparison to salaried employees. As a result, they have to manage tax compliance on their own, from keeping track of their earnings to filing their Income Tax Return (ITR).

It’s important to understand how ITR filing works in order to prevent penalties, make permitted deductions, and maintain a clean financial record.

Who Is Considered a Freelancer for Tax Purposes?

An individual’s earnings from self-employment, skilled work, or artistic skills are subject to taxation under the Income Tax Act of 1961 under the category of “Profits and Gains from Business or Profession.”

Common examples of freelancers include:

- Bloggers, developers, designers, and content creators

- Photographers, trainers, teachers, and consultants

- Professionals such as independent accountants, doctors, advocates, and architects

You are considered a freelancer and are required to file an ITR if you earn money on your own (rather than as a wage).

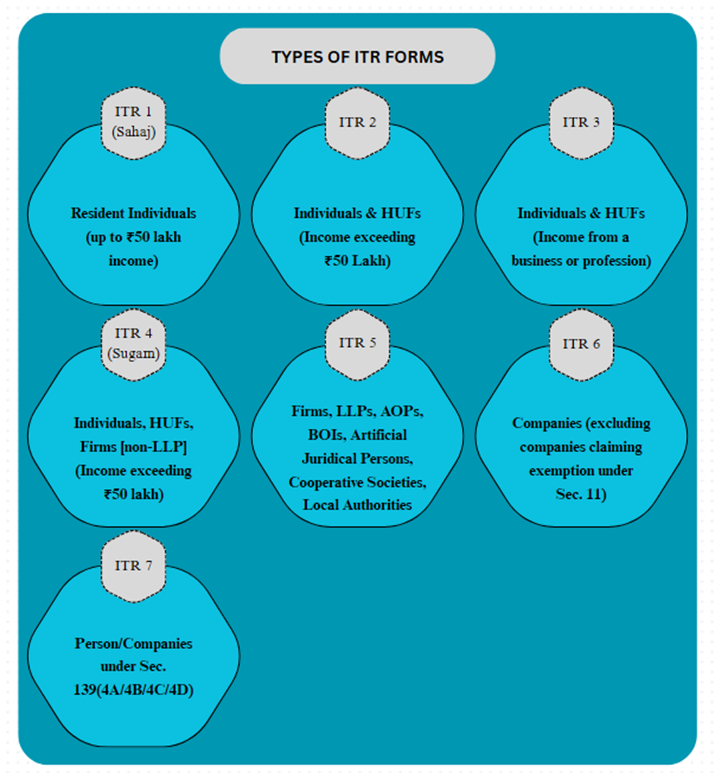

Which ITR Form Applies to Freelancers?

The selection of the right form is the first step in ITR filing:

- ITR-3: Suitable when income is from business or profession without applying for presumptive taxation.

- ITR-4 (Sugam): Used when applying for the Presumptive Taxation Scheme under Section 44ADA, where 50% of the net income is considered taxable. This is allowed if your annual income is up to ₹75 lakh, with cash transactions not exceeding 5%.

Tax Slabs for Freelancers (AY 2025–26)

Freelancers can choose between:

- Old Tax Regime (with deductions)

- New Tax Regime (default, with lower rates but limited deductions)

Click the link to know the Tax Slabs under OLD and NEW TAX Regimes https://taxacumen.in/?p=1056

Deductions Freelancers Can Claim

In case, Freelancers opt for OLD TAX REGIME, there are some deductions to lower their taxable income even though they are not eligible for salary-based exemptions like HRA:

- Section 80C: Investments in PPF, ELSS, life insurance, etc. (limit ₹1.5 lakh).

- Section 80D: Premiums paid for health insurance.

- Section 80E: Interest on education loans.

- Section 80G: Donations to eligible charitable institutions.

- Section 80GG: Deduction for rent paid if no HRA is claimed.

- Business Expenses: Expenses directly related to freelancing, such as home office rent, internet bills, professional equipment, and travel expenses, can be deducted.

These deductions are important for reducing your overall tax liability.

TDS and Advance Tax for Freelancers

Freelancers need to understand their advance tax and TDS obligations as well.

Tax Deducted at Source (TDS): In accordance with Section 194J, clients often deduct 10% TDS from payments. This TDS can be claimed when filing your ITR.

Advance Tax: You must make four payments of advance tax if your total tax liability in a financial year exceeds ₹10,000.

- 15th June – 15% of tax

- 15th September – 45% of tax

- 15th December – 75% of tax

- 15th March – 100% of tax

Non-payment of advance tax results in interest under Sections 234B and 234C.

Important Due Dates for Freelancers (FY 2024–25)

- Advance Tax Instalment – 15th June, 15th September, 15th December, and 15th March

- ITR Filing Deadline – 31st July 2025 (for non-audit cases). The deadline has been extended till 15th September 2025 for the current year only.

Sticking to these deadlines ensures smooth compliance and avoids unnecessary penalties.

Conclusion

Once you understand the basics, filing an ITR as a freelancer is not as difficult as it seems. You can simply maintain compliance by keeping track of your earnings and expenses, selecting the correct ITR form, and making on-time advance tax payments.

Additionally, timely ITR filing improves your financial credibility, helps in refund claims, and simplifies future loan or visa procedures. To take benefits, consider tax filing as a component of your career development and, if necessary, get advice from a tax professional.

Here, this is just a brief about how to know about tax liability, rate slabs, etc for Freelancer. It is also better to consult your Tax consultant before filing ITR

For any further query, connect with us through 91-9267970588 or taxacumen.consultancy@gmail.com