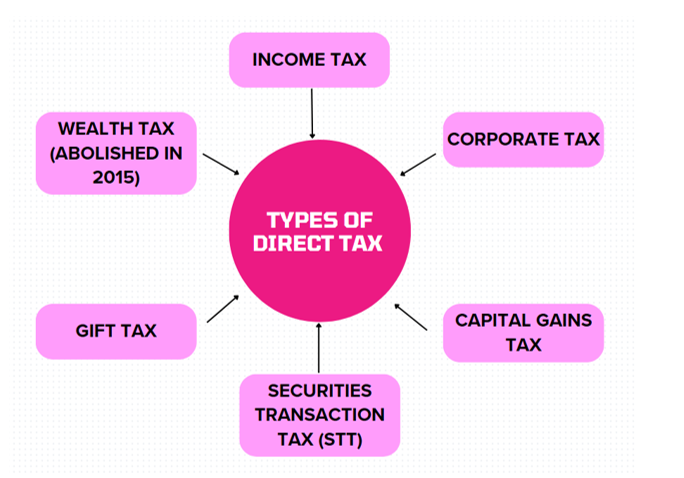

Types of Direct Tax

A Direct Tax is one that is levied upon a person or entity and paid to the government directly. It is impossible to transfer the tax burden to another person.

These are few types of direct tax:

Income Tax (IT)

According to the provisions of the Income Tax Act of 1961, income tax is a tax that is directly imposed on the earnings that individuals, Hindu Undivided Families (HUFs), businesses, limited liability partnerships (LLPs), enterprises, and other entities earn. Five categories are used to categorise the Income: Capital Gains, Profits and Earnings from Business or Profession, Income from House Property, Income from Salaries, and Income from Other Sources. After calculating the relevant deductions and exemptions (such as those provided by Sections 80C, 80D, etc.), tax is due on the total taxable income. Through the Finance Act, the government updates tax rates and slabs every year (Union Budget). The Government of India receives most of its revenue from income tax.

Corporate Tax

According to the Income Tax Act of 1961, Corporate tax is imposed on the net profit of businesses, both local and foreign. While international corporations are only taxed on their income made in India, domestic companies are taxed on their entire income. Under Sections 115BAA and 115BAB, businesses may choose to use concessional rates, subject to specific requirements. Companies may also be required to pay health and education cess and surcharges in addition to corporate tax. India’s revenue is largely derived from corporate taxes, particularly from big businesses in industries like manufacturing, finance, and information technology.

Capital Gains Tax

When Capital Assets, such as buildings, land, gold, shares, and other valuable property, are sold or transferred, the profits are subject to capital gains tax. It is divided into two categories according to the period of time the asset is held: Short-Term Capital Gains (STCG) and Long-Term Capital Gains (LTCG). Depending on the asset type and holding duration, the tax rate changes.

Securities Transaction Tax (STT)

The Securities Transaction Tax (STT) is a direct tax levied on securities-related transactions carried out on authorised stock exchanges, including the buying and selling of shares, derivatives, and equity-orientated mutual funds. In order to streamline the taxes of stock market transactions, it was created by the Finance Act of 2004. Different transaction types have different STT rates. Depending on the nature of the transaction, the buyer, seller, or both may be responsible for paying the tax, which is collected by stock exchanges.

Gift Tax

The 1958 Gift Tax Act served as the original legislation governing gift tax; however, it was repealed in 1998. Gift taxation is now regulated under Section 56(2)(x) of the Income Tax Act of 1961. The amount of gifts given to an individual or HUF in a fiscal year that exceed ₹50,000 in value (apart from certain relatives or exempt categories) is taxed as income from other sources. Some presents, including those given as a marriage present or as an inheritance, are still excluded.

Wealth Tax (Abolished)

A direct tax referred to as wealth tax was imposed on the net worth of specific people, HUFs, and businesses if it beyond the specified amount. It was regulated by the 1957 Wealth Tax Act. Real estate, gold, expensive cars, and jewellery were all subject to wealth tax. The Finance Act of 2015 eliminated wealth tax for the Assessment Year 2016–17 due to the high expenses of compliance and low revenue yield. However, in order to maintain transparency and stop tax evasion, high-value assets are still required to be reported on income tax returns.

Leave a Reply