CAPITAL GAINS TAX IN INDIA – TYPES, TAX RATES & EXEMPTIONS

Capital Gains Tax is a tax imposed on the profits made when a capital asset (capital asset, i.e., property, stock, mutual funds, gold, etc.) is disposed of. Capital gains tax is a significant component of taxation and the tax system in India, affecting both investors and property owners.

The calculation, tax rates and exemptions for capital gains are based on how long the asset is held prior to its disposal. It is important for taxpayers to remain aware of their legal obligations because the budgets presented in Budget 2024 altered a number of capital gains tax rates, indexation, and asset types.

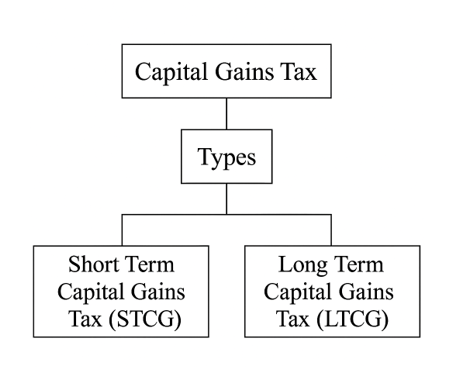

Types of Capital Gains

The types of capital gains are based on how long the asset is held before disposal. Typically, these are classified as 2 types:

Short-Term Capital Gains (STCG)

Short-Term Capital gains apply when the asset is sold in a short amount of time. The holding period depends on how the asset is held:

- For listed shares and equity mutual funds, where sold in 12 months

- For unlisted shares and properties, where sold in 24 months

- For other assets, such as gold, bonds, etc., which were sold in 36 months

Compared to long-term gains, the tax rate on profits from such sales is higher. Recent changes have raised the STCG tax rates for mutual fund redemptions and listed equity shares in an attempt to prevent speculation and short-term trading.

Long-Term Capital Gains (LTCG)

If the asset is held over and beyond the short-term thresholds discussed above, any profit on the sale of the asset would be treated as a long-term capital gain. The holding periods are:

- Over 12 months for listed equity shares and mutual funds

- Over 24 months for unlisted shares and immovable property

- Over 36 months for all other assets

LTCG will generally be taxed at lower rates than STCG. The only disadvantage is that for the sale of most assets, indexation will be eliminated for sales after July 23, 2024.

Capital Gains Tax Rates (FY 2025–26)

The tax rates that apply are shown below:

| Asset Type | Holding Period | Tax Rate |

| Listed Equity Shares & Equity Mutual Funds | Short-Term (≤ 12 months) | 20% (previously 15%) |

| Long-Term (> 12 months) | 12.5% on amounts above ₹1.25 lakh | |

| Unlisted Shares & Real Estate | Short-Term (≤ 24 months) | Taxed as per slab |

| Long-Term (> 24 months) | 12.5% without indexation | |

| Gold, Bonds, Debentures, Other Assets | Short-Term (≤ 36 months) | Taxed as per slab |

| Long-Term (> 36 months) | 12.5% without indexation |

Note: Because most long-term assets were sold after July 23, 2024, indexation has been removed.

Exemptions on Capital Gains Tax

The Income Tax Act has exemptions for reinvestment of capital gains in certain sections:

Section 54: Exemption on the sale of residential property if reinvested in another house.

Section 54F: Exemption on the sale of any long-term capital asset if the sale profits are reinvested in a house.

Section 54EC: Exemption allowed if the profits are invested in specified bonds within 6 months of sale.

The Capital Gains Account Scheme (CGAS) can be used to temporarily store the sale profits in case immediate reinvestment is not possible.

Conclusion

Capital Gains Tax (CGT) plays a vital role in wealth management and decision-making in investing. It is critical to understand the difference between short-term capital gains and long-term capital gains so tax liabilities can be planned accordingly.

With the recent tax changes, some careful investment planning and holding periods beyond short-term assets and all the exemptions as per the new laws may reduce tax liability.