TYPES OF ITR – INCOME TAX FORMS

Income Tax Return is referred to as ITR. Different Income Tax Return (ITR) forms have been provided by the Indian Income Tax Department for different taxpayer categories. Every form is made according to the taxpayer’s category and the type of income. For compliance, accurate tax assessment, and penalty avoidance, it is essential to file the correct ITR form.

An Income Tax Return (ITR) is a form that taxpayers submit to the income tax department stating their earnings and any necessary taxes.

Till now, the department has issued seven forms. It is essential that all taxpayers submit their ITRs before the due date. ITR forms are applicable in many ways depending on the taxpayer’s income sources, income amount, and taxpayer category (individuals, HUF, firm, etc.).

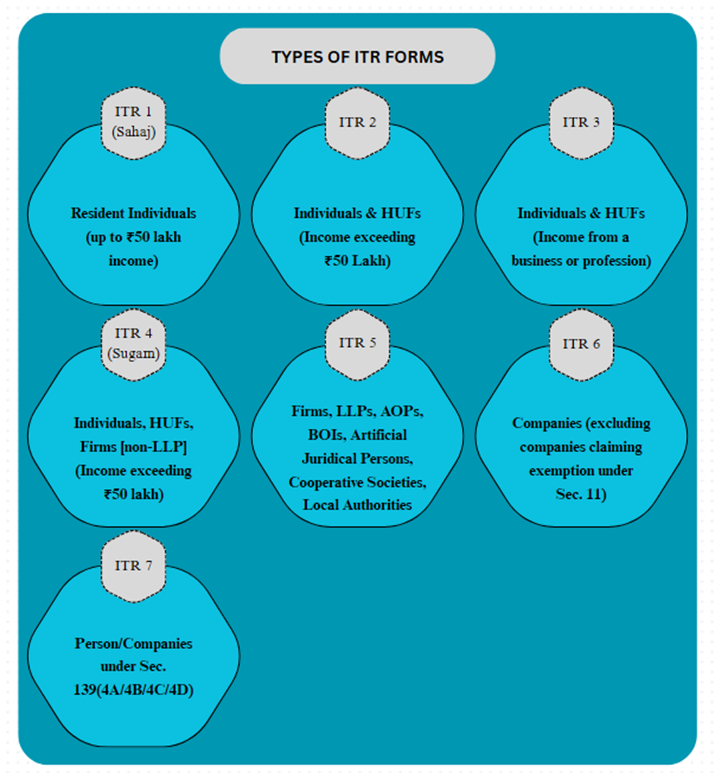

ITR – 1 (SAHAJ)

The ITR-1 has been designed for residents with annual incomes up to ₹50 lakh. It can be applied if sources of income consist of:

- Pension or salary

- Income from a single property (unless there is a carried loss)

- Other sources of income (not include prizes from horse racing or the lottery)

- Income from agriculture up to ₹5,000

- Section 112A allows for long-term capital gains of up to ₹1.25 lakh without carrying forward losses

However, anyone with business or professional income, multiple home properties, capital gains that exceed certain restrictions, overseas assets or income, directorship in a corporation, or investments in unlisted equity shares are not permitted to use ITR-1.

ITR – 2

Individuals and HUFs without business or professional income are subject to ITR-2. It works well if your earnings include of:

- Pension or salary

- Revenue from residential real estate, including multiple properties

- Capital gains

- Foreign assets and income

- Agricultural earnings that exceed ₹5,000

- Other sources of income, such as winners from horse racing and the lottery

If you have unlisted equity shares, are a Resident Not Ordinarily Resident (RNOR), are a non-resident, or are a director of the company, you must file an ITR-2. This form is not intended for people who make a living through their profession or company.

ITR – 3

Individuals and HUFs with business or professional income are required to file ITR-3. It includes the following:

- Private businesses or occupations (where an audit is required or books of accounts are maintained)

- Income from partnerships (as a partner in a firm)

- earnings from capital gains, real estate, salaries, and other sources

ITR-3 is the appropriate form to use if your income comes from a proprietary business or occupation that is not subject to presumed taxes.

ITR – 4 (SUGAM)

Individuals, HUFs, and businesses (except from limited liability partnerships) that choose presumptive taxes under Sections 44AD, 44ADA, or 44AE and are residents are subject to ITR-4. It can be applied if:

- Up to ₹50 lakh is the total income

- Sections 44AD or 44AE are used to declare business income

- Section 44ADA’s definition of professional income

- income from a job, a single residence, or other sources (not including prizes from horse racing or the lottery)

This form is also available to freelancers with gross incomes up to ₹50 lakh. However, if you have income beyond ₹50 lakh, own foreign assets, or are a director of a corporation, you cannot use ITR-4.

ITR – 5

ITR-5 is meant for:

- Firms

- LLPs

- AOPs (Association of Persons)

- BOIs (Body of Individuals)

- Artificial Juridical Persons

- Estate of deceased or insolvent persons

- Business trusts and investment funds

ITR-5 should be filed by entities that must report income, excluding corporations and trusts.

ITR – 6

Companies are regulated by ITR-6, with the exception of those that assert an exemption under Section 11 (charitable/religious reasons). This return must be submitted electronically by businesses using a digital signature.

ITR – 7

ITR-7 is used by institutions, political parties, trusts, and other organisations that must file returns under:

- Section 139(4A): Trusts and legal obligations for charitable/religious purposes

- Section 139(4B): Political parties

- Section 139(4C): News agencies, scientific research associations, educational and medical institutions

- Section 139(4D): Universities and colleges

- Section 139(4E) & (4F): Business trusts and investment funds

WHY SHOULD YOU FILE ITR?

In addition to being required by law, submitting an ITR offers the following benefits:

- helps in obtaining income tax refunds

- Necessary for loan and visa applications

- allows capital or commercial losses to be carried forward

- serves as evidence of income

- required for businesses, including those with little profit

CONCLUSION

The type of income, the taxpayer category, and the income level all affect which ITR form is appropriate. Rejection or penalties may follow the submission of an inaccurate form.

Here, this is just a brief about how to know which ITR Form is applicable to you based on your income structure. Consult your Tax consultant before opting for ITR Form or connect with us through

91-9267970588 or taxacumen.consultancy@gmail.com

Leave a Reply